Plastic, notable for its durability, lightness and efficiency, plays a crucial role in various sectors, including medicine, the automotive industry and construction, providing a lower environmental impact compared to other materials.

Once considered a villain, the sector has adapted to the demands of sustainability so that plastic, in the vast majority of cases, is recyclable and allows the incorporation of materials already used in its production, such as PETs.

Another advantage for the environment is that it requires fewer natural resources in its production and uses by-products from the petrochemical industry, optimizing the use of raw materials and energy used in oil extraction.

In the health sector, the importance of plastic is undeniable, as it allows for the manufacture of highly resistant, low value equipment, and is present in many hospital goods such as goggles, syringes, gloves and many others.

These nuances of the sector demonstrate its importance and justify various tax benefits granted over the years, as well as explaining the need for it to receive differentiated treatment even after the Tax Reform.

As you know, the sector has numerous tax benefits that are justified by the undeniable importance of its products, which perform important functions for the food, pharmaceutical, automotive and engineering industries, etc.

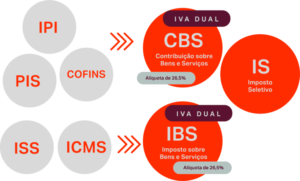

Check out a basic illustration of what the current tax system looks like and what it looks like after the reform!

It is important to note that PLP 68/2024 is responsible for instituting the Tax on Goods and Services, the Social Contribution on Goods and Services and the Selective Tax. The basic text approved included an estimated 26.5% tax rate lock (CBS + IBS), following the Value Added Tax (VAT) model.

Impact of the Tax Reform on the plastics sector

The approved Tax Reform confirmed the move to put an end to special and/or differentiated regimes and this has caused concern for the sector’s industries.

It is worth remembering that the reform provides for a reduction in the IBS and CBS rates for products intended for human consumption that will make up the National Basic Food Basket.

As such, the sector will not be negatively affected by the reform, given that plastic has the capacity to store and extend the useful life of products in the food sector.

On a positive note, we have the implementation of full non-cumulative taxation, which allows tax credits to be used in full, and this could bring benefits to industries in the plastics sector. This is the foundation of the Tax Reform, aimed at reducing the cascading effect and making the tax environment more predictable and equitable.

Points of attention

The Tax Reform also includes the creation of the Selective Tax – IS, which will be levied on the production, extraction, sale or import of goods and services that are harmful to health or the environment.

Considering all the care the sector takes with the environment, as already mentioned, it is hoped that it will not be subject to this new tax, since during its industrialization it does not have significant impacts on the environment.

So far, this sector has not been included in the scope of the IS, but this does not mean that it is free from this tax, as there is an express constitutional provision on the possibility of this tax being levied.

The IS, also known as the “sin tax”, if applied to the plastics sector, can cancel out the reductions granted to other sectors. In other words, if there is a tax increase in the sector through the Selective Tax, there will consequently be a revocation of the benefits of the rate reduction for other segments, as it will increase production costs.

Main changes compared to the current system

Below is a table summarizing the main changes brought about by the Tax Reform compared to the current system.

Conclusion

It is prudent to remain moderately cautious about the reform, even though it proposes a promising scenario, the implementation of the changes and the maintenance of the effective tax burden will still require careful observation and assertive fiscal management.

The discussions are not yet closed, but one thing is certain: understanding the issues being addressed must be a priority for companies that want to prepare for the next stages of the Tax Reform.

Did you enjoy the content? We hope it has clarified what will change in the plastics sector with the Tax Reform.

If you have any questions, click here and talk to our team of experts.